The latest KLAS Digital Pathology 2026 Report reveals significant growth in the U.S. digital pathology market, driven by recent FDA clearances and advancements in reimbursement structures. Despite this progress, fewer than 15% of healthcare organizations in the United States have adopted a digital pathology vendor, indicating that the field is still in its nascent stages.

Leading Vendors in Image Management Systems

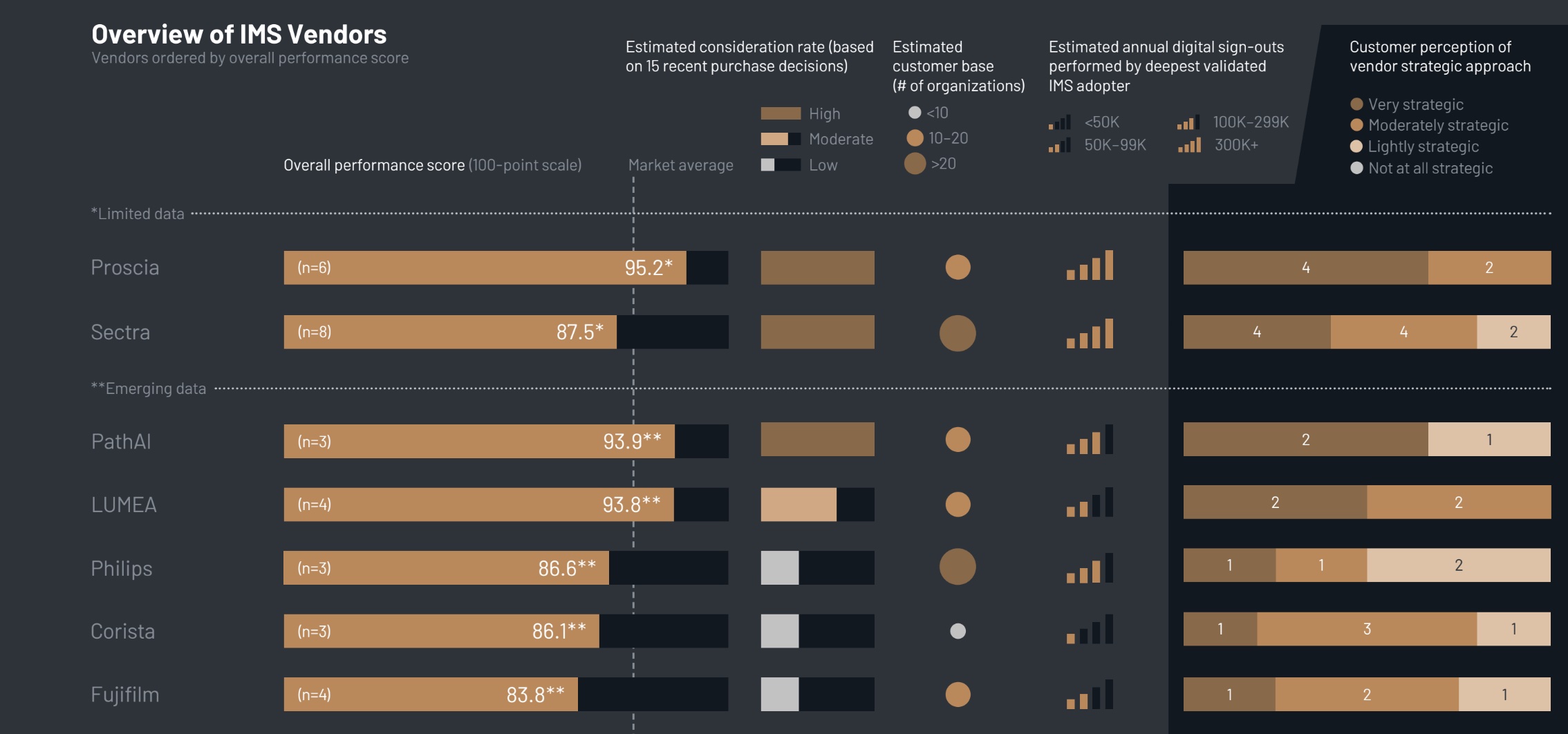

The report identifies key players in the Image Management Systems (IMS) sector, where pathology-specific vendors such as Proscia, PathAI, and LUMEA are outperforming traditional radiology providers in terms of customer satisfaction. Users have expressed appreciation for the tailored solutions and strategic support offered by these companies.

Leica Biosystems stands out as the dominant force in the U.S. clinical scanner market. Customers consistently highlight its reliable scanning capabilities, efficient slide loading, and consistent performance. In contrast, users of Roche scanners report dissatisfaction due to reliability issues and inadequate throughput, which hinder workflow efficiency.

Hospitals are increasingly evaluating AI technologies for clinical applications, particularly focusing on algorithms for breast and prostate cancer. A crucial requirement for these AI tools is their ability to integrate smoothly into the IMS workflow, rather than operating as standalone systems.

The Divide: Specialists vs. Generalists

The KLAS report highlights a clear divide in the IMS market between established radiology vendors that have expanded into pathology—like Sectra, Philips, and Fujifilm—and newer, pathology-specific vendors. Currently, specialists are leading in customer satisfaction.

Proscia has become the most considered IMS vendor, with clients praising its collaborative, education-focused approach. Meanwhile, PathAI has garnered positive feedback for its proactive communication and hands-on integration efforts. Customers of LUMEA commend the platform’s user-friendliness and the vendor’s commitment to adapting workflows to meet specific needs.

Despite the rapid growth of traditional imaging vendors like Sectra, some customers have noted that post-implementation support feels limited. As organizations mature, there is a growing demand for proactive guidance, particularly concerning AI interoperability.

The report underscores the essential role of scanner hardware in the digital pathology landscape. Leica Biosystems, a pioneer in obtaining FDA clearance for its Aperio GT 450 DX scanner, remains the most widely adopted solution in clinical settings across the U.S. Users describe its high-quality imaging and reliable performance as key advantages that enhance productivity.

Conversely, many users of Roche scanners have voiced concerns regarding reliability and throughput, which disrupt their high-volume diagnostic workflows.

The increasing interest in AI technologies is reshaping the digital pathology landscape. Organizations are no longer merely researching AI; they are actively assessing its clinical applications. Among the most sought-after areas for AI implementation are breast cancer algorithms that facilitate biomarker assessments, such as Ki-67, HER2, estrogen receptor (ER), and progesterone receptor (PR) evaluations.

Top AI vendors under consideration include Ibex, Visiopharm, Paige.ai, and PathAI. A crucial demand from buyers is that AI solutions must integrate seamlessly into the IMS workflow. Respondents emphasize the necessity for AI to function as part of routine clinical operations, rather than requiring pathologists to navigate separate systems.

For further details on the findings, visit KLAS Research.